Cheapest Rural Property in the UK: Where to Buy in 2026

Photo by Erik Odiin on Unsplash

The cheapest local authority in Britain is Inverclyde at around £113,000, with Burnley the cheapest in England near £129,000. Where to find cheap rural houses for sale in 2026 — and how to buy one safely.

The cheapest rural properties in the UK are concentrated in the north of England, Scotland, and Wales. The cheapest local authority in Britain is Inverclyde at around £113,000 (HM Land Registry/ONS, March 2026), and the cheapest in England is Burnley at about £129,000. For genuine countryside character, the strongest value sits in County Durham (around £138,000), Cumberland in west Cumbria, Dumfries & Galloway (around £138,000), East Ayrshire, and parts of Wales — typically well below comparable southern homes. The trade-offs are fewer local amenities and more legal due diligence: access rights, agricultural ties, and off-grid utilities all need checking. This guide shows exactly where to find cheap rural houses for sale in 2026 and how to buy one safely.

The UK rural property market offers real opportunities for buyers willing to work through its complexities. With rural properties continuing to outperform urban areas over the past five years, countryside living offers both lifestyle benefits and investment potential. Success requires understanding regional variations, specialised resources, and the legal side of rural property ownership.

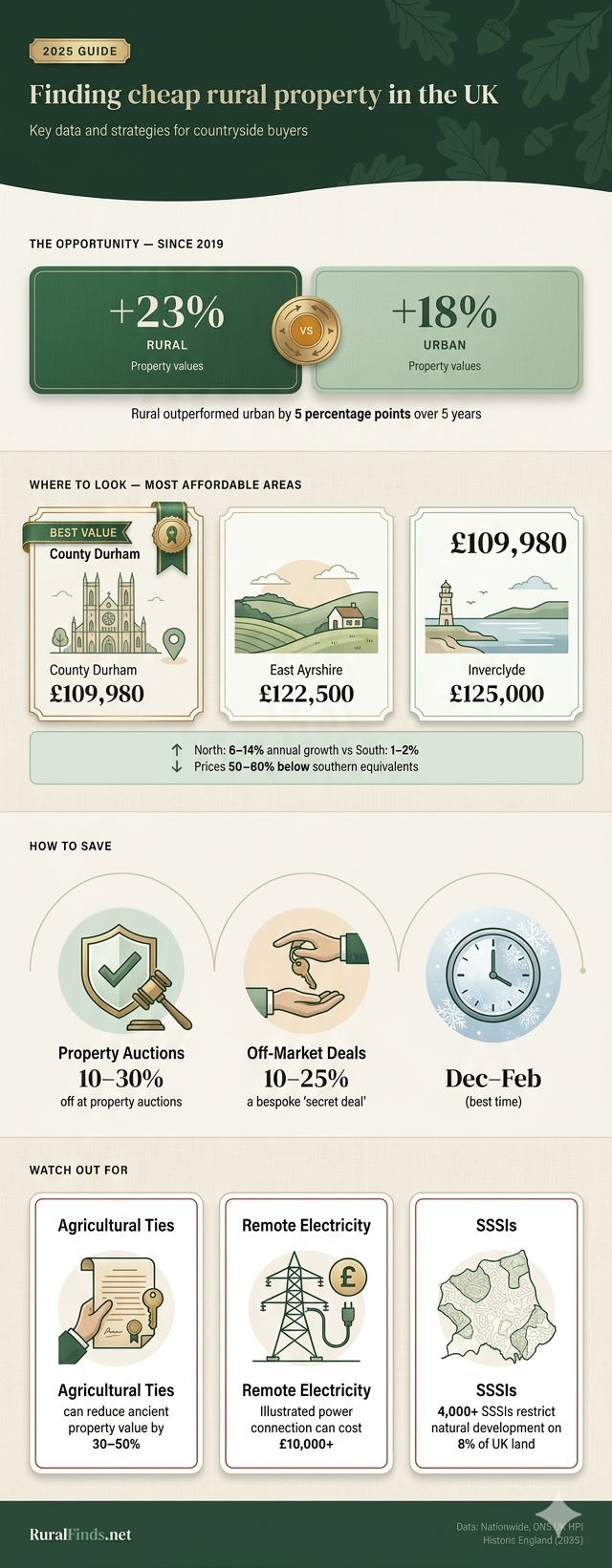

According to Nationwide, house prices in predominantly rural areas rose 23% between December 2019 and December 2024, compared with 18% in predominantly urban areas — a roughly 5-percentage-point edge that reflects sustained demand for countryside living. Yet there are wide regional variations, and buyers can still find strong value in the right locations.

Current market dynamics favour strategic rural buyers

The headline market has cooled. UK house-price growth was effectively flat in early 2026 — 0.0% in the year to March 2026 on the official HM Land Registry/ONS index, and 1.7% in May 2026 on the Nationwide index — down sharply from the 3%-plus readings of a year earlier. That softness is partly a base effect from the April 2025 stamp-duty change, which pulled transactions forward into early 2025. For buyers, a flat, well-stocked market means more choice and more room to negotiate.

The North–South divide that underpins rural value remains firmly in place. The fastest growth in early 2026 was in Northern Ireland (around +7–9.5%), the North West (around +3%), and Scotland and Wales, while London and much of the South were flat to slightly falling. This continues to create clear geographic opportunities for buyers willing to look beyond traditional rural hotspots like the Cotswolds and Devon.

On affordability, Inverclyde is Britain’s cheapest local authority at around £113,000, and Burnley is the cheapest in England at about £129,000. Among areas with genuine rural character, County Durham averages around £138,000, Cumberland (the new unitary authority covering the former Copeland and Allerdale districts of west Cumbria) around £170,000, and Dumfries & Galloway — the cheapest predominantly rural area in Scotland — around £138,000. These areas combine countryside character with prices well below southern equivalents, while still offering modern amenities and connectivity.

Note on local figures: Local-authority averages are based on small monthly samples and move around. The numbers above are drawn from the HM Land Registry/ONS UK House Price Index for late 2025 to spring 2026; always check the latest monthly release for your target area before making decisions.

A new factor for 2026: the inheritance-tax reform on farms and land

The single biggest change to the rural market in 2026 is a reform to Agricultural Property Relief (APR) and Business Property Relief (BPR) for inheritance tax, which takes effect from 6 April 2026.

Until now, qualifying farmland and farming businesses could be passed on with up to 100% relief from inheritance tax. From April 2026, full 100% relief is capped at £2.5 million per person (raised from the £1 million figure originally proposed in the Autumn 2024 Budget, after a revision announced on 23 December 2025). Value above the cap qualifies for 50% relief, giving an effective inheritance-tax rate of 20% on the excess. The £2.5 million allowance is transferable between spouses and civil partners, so a couple can pass on up to £5 million (and more once the standard nil-rate bands are included).

HM Treasury estimates the reform will affect a relatively small number of estates — up to around 1,100 estates a year, of which roughly 185 claim agricultural relief — but its effect on sentiment has been significant. Through 2025, publicly marketed farmland supply actually fell by around 16% as owners paused decisions, and farmers themselves made up more than half of all buyers. The December 2025 uplift to £2.5 million restored a good deal of confidence, and some agents (Savills among them) expect a gradual increase in land coming to market from 2027 as families plan around the new rules.

For buyers of cheap rural homes, the practical takeaways are: working farms and large landholdings now carry a succession-planning consideration they did not before; this may bring more land and farm property to market over the next few years; and anyone buying agricultural land or a working holding should take specialist tax advice before committing. For a modest cottage or smallholding, the reform is unlikely to bite directly, but it is reshaping the wider supply picture.

Specialised platforms unlock hidden rural property deals

Beyond mainstream portals like Rightmove and Zoopla, UK Land & Farms is a leading specialised platform for rural properties over 3 acres. This dedicated resource features farms, agricultural land, equestrian properties, and country estates often missed by general buyers.

Rural Scene, operating since 1994, offers personalised service connecting buyers with equestrian properties, farms, and smallholdings across England, Wales, and Scotland. Their specialist approach means access to properties rarely advertised elsewhere, particularly useful for buyers seeking unusual rural opportunities.

The most successful rural property hunters register with multiple specialist agents including Savills Rural, Knight Frank Farms & Estates, and Strutt & Parker’s rural division. These agents handle exclusive off-market opportunities and understand agricultural law, planning permissions, and financing options.

Regional specialists bring deeper local knowledge and community connections. Halls Rural Professional covers traditional farming regions like Shropshire and Worcestershire well, while C&D Rural, GSC Grays and (in Scotland) Galbraith and Carter Jonas dominate their local patches. Building relationships with these specialists often reveals opportunities before they reach public markets.

For straightforward price research, the free HM Land Registry sold-price tool (and Registers of Scotland north of the border), alongside the sold-price data on Rightmove and Zoopla, lets you check what comparable rural homes have actually achieved rather than relying on asking prices.

Property auctions can secure value — with realistic expectations

Property auctions remain one of the more reliable ways to buy below the open market, but the discounts need framing carefully. Major auction houses like Auction House, Clive Emson, SDL Auctions and Allsop regularly feature rural properties needing renovation or quick sale.

Guide prices are typically set 10–20% below the reserve or expected sale price, deliberately, to attract bidding — so lots commonly sell above their guide. The realised discount to genuine market value is usually smaller than the guide-to-sale gap suggests. As a rule of thumb, genuine below-market-value deals run around 15–25% below open-market value; anything advertised as a 30%-plus discount almost always carries a hidden problem (structural issues, legal complications, or a restrictive tie).

Buyers have also become more disciplined: the share of homes selling 30% or more above guide has fallen from around 27% in 2021–22 to roughly 19% in 2025–26. The advantages of auction remain real, though — transparent pricing, immediate exchange of contracts, and no gazumping risk — and most houses now offer telephone, internet, and proxy bidding, making participation accessible from anywhere.

Successful auction buyers do thorough pre-sale research including legal-pack analysis, structural surveys, and financing arrangements before they bid, because exchange happens on the fall of the hammer. Properties needing renovation achieve the steepest discounts, with meaningful savings against renovated equivalents — but only for buyers who have priced the works accurately.

Off-market opportunities require systematic networking

Some of the better rural discounts come from off-market transactions, often around 15–25% below open-market value where a seller is genuinely motivated. Direct mail campaigns targeting property owners in desired postcodes generate consistent responses from sellers avoiding public marketing costs and competition. (Note that since October 2023, property deal-sourcers in England must be registered with a redress scheme and follow anti-money-laundering rules — worth checking if you use a sourcing agent.)

Building relationships with local estate agents creates access to properties before public listing. Many agents maintain private databases of potential sellers and match them with registered buyers before advertising begins. This approach requires patience but consistently produces better deals.

Rural communities offer unique networking opportunities through parish councils, village events, agricultural shows, and local businesses. Pub landlords, farm suppliers, and veterinarians often know about coming property sales months before they reach the market. Regular visits to target areas and genuine community engagement build valuable information networks.

The “three D’s” (debt, divorce, and death) drive most distressed property sales. Monitoring probate records, building solicitor relationships, and tracking business difficulties help identify motivated sellers who need quick transactions.

Strategic timing in a buyer-friendly market

The conventional wisdom that winter (December–February) is the best time to buy still holds up reasonably well: there is less competition, and some sellers face year-end or personal pressures. Rural properties are also harder to view and assess in winter, which deters casual buyers while creating openings for serious ones, and homes returning to market after failed summer sales often come with more realistic sellers.

That said, the bigger timing story in 2026 is not the season but the backdrop. For-sale stock is unusually high — Rightmove has recorded the most homes per agent for the time of year in over a decade — which tilts negotiating power toward buyers in most regions regardless of the calendar.

Economic timing matters too. Interest-rate moves, local employment disruptions, and agricultural market fluctuations create motivated sellers in specific regions. Keeping an eye on these factors helps identify emerging opportunities before they become obvious to other buyers.

Legal complexities need specialist professional guidance

Rural property purchases involve legal issues rarely encountered in urban transactions. Agricultural occupancy conditions (agricultural ties) restrict occupancy to people working (or last working) in agriculture, typically reducing values by around 25–30%, occasionally up to 40%. That discount is a genuine opportunity for qualifying buyers — but a serious constraint on resale and financing for everyone else.

Planning permissions and permitted development rights offer real value-creation potential, and the rules changed materially in 2024. Following reforms that took effect on 21 May 2024, Class Q now allows the conversion of agricultural buildings to up to 10 dwellings (previously 5), within a total of 1,000 m² and a 150 m² cap per dwelling, and it now covers former agricultural buildings (provided they were part of an agricultural unit on or before 24 July 2023). A suitable existing or achievable highway access is now required, and — importantly — Class Q does not apply in National Parks or National Landscapes (formerly AONBs). Class R, which allows flexible commercial conversions, was expanded to 1,000 m² and now includes sport, recreation and certain other uses. The transitional window to apply under the old rules closed on 20 May 2025, so any new application now follows the updated regime.

Agricultural Holdings Act tenancies create complex landlord–tenant relationships affecting property values and usage rights. Pre-1995 tenancies offer lifetime security of tenure, while newer Farm Business Tenancies give landlords more flexibility. Professional legal advice is needed to understand existing obligations and rights.

Listed building considerations add another layer. England’s listed buildings — more than 370,000 entries on Historic England’s National Heritage List — require special consent for alterations but often qualify for heritage grants and tax reliefs. Understanding maintenance obligations and development restrictions before purchase is essential.

Stamp duty: what changed in 2025

Buyers should budget for the Stamp Duty Land Tax (SDLT) thresholds that took effect in England and Northern Ireland on 1 April 2025. The nil-rate threshold fell from £250,000 to £125,000, and the first-time-buyer threshold fell from £425,000 to £300,000 (with relief now available up to a £500,000 purchase price).

The good news for budget-conscious rural buyers is that most of the cheapest rural homes — those under £125,000, and certainly the sub-£140,000 bargains across the north of England, Scotland and Wales — fall at or near the bottom of the SDLT scale. (Scotland and Wales operate their own systems: Land and Buildings Transaction Tax and Land Transaction Tax respectively, each with its own thresholds.) No further SDLT changes have been announced for 2026, but it is worth confirming current rates with your solicitor at the point of purchase.

Financing rural properties demands specialised lenders

Traditional high-street lenders are often cautious about properties with agricultural ties or significant acreage, and many decline tied properties outright or cap the land they will lend against. Specialist rural lenders — including Oxbury Bank, the Agricultural Mortgage Corporation (AMC, part of Lloyds), Virgin Money, and agricultural departments within the major banks — understand countryside property financing.

It is worth correcting a common misconception: true agricultural mortgages typically cap at around 70% loan-to-value (a 30% deposit), with rates generally in the 6–7.5% range. The much higher loan-to-values sometimes advertised apply to unrestricted residential smallholdings that a lender treats as an ordinary home, not to working farms or tied properties. The key to securing finance is demonstrating income stability and property value through detailed business plans and professional valuations.

Offset mortgages work particularly well for rural buyers with variable incomes from farming, tourism, or seasonal businesses, letting surplus cash offset mortgage interest while keeping funds accessible. Bridge financing often proves necessary for auction purchases or quick completions, and specialist rural finance brokers can navigate complex lending requirements.

On rates more broadly: the Bank of England base rate stands at 3.75% in mid-2026, and — against earlier expectations of steady cuts — the outlook has become less certain, with markets pricing the possibility of holds or even modest rises following an energy-driven uptick in inflation. Average two-year fixes sit around 4.5–4.8% and five-year fixes around 4.9%. Buyers should stress-test affordability against rates staying higher for longer rather than assuming further falls.

Due diligence needs thorough rural-specific checks

Rural property purchases demand extensive due diligence beyond standard residential surveys. Boundary surveys by RICS-qualified professionals are essential, since Land Registry plans show only general boundaries for rural properties, creating higher dispute risks.

Access rights and easements require careful investigation. Legal access via adopted roads, private road maintenance responsibilities, utility easements, and agricultural access rights for large machinery can all affect property usage and costs.

Environmental searches identify Sites of Special Scientific Interest (SSSI), Tree Preservation Orders, and protected species habitats affecting development rights. England’s 4,100-plus SSSIs cover around 8% of the country’s land area and impose strict restrictions on damaging activities.

Utility availability presents real challenges in remote locations:

- Electricity connections start at around £10,000 for a typical rural connection and can reach £20,000–£100,000-plus where new poles, transformers, trenching or wayleaves are required. Quotes are site-specific, from your regional Distribution Network Operator.

- Private water from a borehole typically costs around £8,000–£15,000 (budget £12,000–£14,000 as a realistic starting point), rising to £25,000–£35,000 in difficult ground. Large abstraction (over 20,000 litres a day) requires an Environment Agency licence, and supplies need regular quality testing.

- Septic tanks and package treatment plants must meet the General Binding Rules. A tank discharging directly to a watercourse must be replaced or upgraded, and on sale, buyer and seller must agree who is responsible for any non-compliant system. Replacement runs from a few thousand pounds for a basic tank to £6,000–£15,000-plus for a treatment plant.

- Broadband is improving fast: around 90% of UK premises could access gigabit-capable broadband by spring 2026 under Project Gigabit, with a target of 99% by 2032. But rollout to the hardest-to-reach rural premises is uneven and some contracts have slipped, so always check the official gigabit address checker and consider satellite (Starlink), 4G/5G or fixed-wireless as a fallback before you commit.

Renovation opportunities multiply investment returns

Properties needing renovation consistently offer the highest discounts in rural markets. Overgrown gardens, boarded windows, and dated interior photos all help identify opportunities that other buyers overlook.

David and Heather Burton’s cottage project shows typical renovation potential: they purchased a 200-year-old cottage via sealed bid in severe disrepair, then transformed it through systematic renovation focusing on structural integrity first, then cosmetic improvements.

Luke Thomas’s Welsh cottage project shows innovative approaches to rural renovation. By reversing the property layout to make the most of garden views and adding a lean-to kitchen conservatory, he created flexible living space suited to modern needs while respecting traditional character.

Energy-efficiency improvements offer both immediate benefits and long-term value. Government grants support heritage building restoration, while modern insulation and heating systems cut ongoing costs in draughty period properties. Buyers who would rather not take on a multi-year renovation increasingly choose prefab and modular homes instead, putting a new energy-efficient house on a cheap rural plot in a matter of months.

Regional variations create clear investment strategies

Northern England and Scotland offer the strongest value for rural property investment. County Durham, at around £138,000, remains exceptional value for countryside living with heritage appeal and community infrastructure, while Cumberland in west Cumbria offers traditional Lakeland-fringe character at around £170,000.

Scottish Highlands and Borders regions provide remote countryside character at competitive prices, though buyers must weigh access challenges and infrastructure limitations. The balance between remoteness and practical necessities like broadband and healthcare access is the key consideration.

Dumfries & Galloway — the cheapest predominantly rural area in Scotland, at around £138,000 — shows Scottish rural value well, offering former dairy-farm conversions, coastal properties with development potential, and traditional stone cottages in village settings. Agricultural land with conversion possibilities creates additional value.

Welsh valleys offer some of Britain’s most affordable countryside: Blaenau Gwent is the cheapest local authority in Wales (around £140,000), and areas such as Merthyr Tydfil combine good landscapes with low prices. Powys, by contrast, is one of Wales’s more expensive rural authorities at around £237,000 — beautiful, but a reminder that “rural” does not automatically mean “cheap.” As ever, understand local employment markets and transport links before committing.

Success requires a systematic approach

The most successful rural property buyers combine multiple strategies. Register with 3–5 specialist agents in target regions while keeping active searches running on specialised platforms.

Build your professional team — rural solicitors, agricultural surveyors, specialist mortgage brokers — before beginning serious property searches. These relationships prove essential for quick decision-making when opportunities arise.

Establish a regular presence in target areas through community events, local business relationships, and area exploration. Rural property success often depends on local knowledge and timing that only come from consistent engagement.

Monitor public records including probate filings, planning applications, and Land Registry changes to spot emerging opportunities before they reach broader markets.

The rural property market rewards preparation, patience, and professional guidance. While the complexities exceed urban property investment, the combination of lifestyle benefits, value-growth potential, and discount opportunities makes rural property investment attractive for buyers willing to master its particular requirements.

Current market conditions favour rural buyers who understand regional variations, use specialised resources, and work systematically. From sub-£140,000 cottages across the north of England, Scotland and Wales to renovation opportunities throughout the UK, there is strong rural value for prepared buyers willing to work through the countryside market’s distinctive challenges.

Essential Resources for Rural Property Buyers

Specialised Property Platforms:

- UK Land & Farms - Leading platform for rural properties over 3 acres

- Rural Scene - Specialist equestrian and farming properties

- Property Auctions UK - Rural auction opportunities

Professional Services:

- Savills Rural - Premium rural property specialists

- Agricultural Mortgage Corporation (AMC) - Agricultural and rural mortgage specialists

- Historic England - Listed building guidance

Government Resources:

- UK House Price Index - Official price data

- Protected Areas Guidance - Environmental restrictions

- Agricultural Property Relief changes - Inheritance-tax reform from April 2026

- Agricultural Tenancy Information - Legal framework guidance

Corrections and updates

This guide was first published in June 2025 and last updated on 12 June 2026. In the latest update we revised the following:

- Cheapest-area figures. Earlier versions named County Durham (£109,980) as the UK’s cheapest area. On the latest HM Land Registry/ONS data, the cheapest local authority in Britain is Inverclyde (around £113,000) and the cheapest in England is Burnley (around £129,000); County Durham now averages around £138,000. All regional prices have been re-dated to late-2025/spring-2026 figures.

- Copeland. References to “Copeland (Cumbria)” have been corrected: Copeland was abolished in April 2023 and is now part of the Cumberland unitary authority.

- House-price growth. The previously cited nationwide growth figure (3.5%) has been updated to the current readings (0.0% on the HM Land Registry index to March 2026; 1.7% on the Nationwide index to May 2026).

- Agricultural mortgages. The earlier statement that agricultural mortgages reach “up to 95% loan-to-value” has been corrected: true farm mortgages typically cap at around 70% LTV; higher figures apply only to unrestricted residential smallholdings.

- Agricultural-tie discount. Figures have been standardised to “around 25–30%, occasionally up to 40%,” replacing an earlier inconsistent range (20–40% / 30–50%).

- New material added for 2026: the Agricultural and Business Property Relief inheritance-tax reform (effective 6 April 2026), the April 2025 Stamp Duty Land Tax threshold changes, the post-21 May 2024 Class Q/Class R permitted-development rules, the current Bank of England base rate, and Project Gigabit broadband progress.

Local-authority averages are based on small monthly samples and can change; always check the latest UK House Price Index release for your target area before making decisions.

Frequently Asked Questions

What is the cheapest place to buy rural property in the UK? +

Are rural property auctions cheaper than buying through an estate agent? +

Can you get a mortgage on a cheap rural property? +

What checks should I do before buying a cheap rural house? +

Why are some rural properties so cheap? +

Infographic: Finding Cheap Rural Properties in the UK: Key Strategies and Opportunities

Click the image or the button above to download. Feel free to share this infographic with attribution.

Related guides

- Agricultural Ties on Rural Property: How to Remove One (2026)An agricultural tie can cut value 20–40%. How agricultural occupancy conditions work, who qualifies, and how to remove a tie — explained for 2026.

- Private Road Maintenance Responsibilities in the UK: 2026 Legal GuideWho is legally responsible for maintaining a private road or access drive in the UK? Duties, costs, and easement rules across England, Scotland, Wales & NI.

- Septic Tank Regulations UK 2026: Complete Compliance GuideSeptic tank regulations in the UK for 2026: General Binding Rules, discharge limits, selling rules, and £100,000 fines for England, Scotland, Wales & NI.

- Borehole Installation in the UK: Costs & Complete 2026 GuideWhat does a borehole cost in the UK? A 2026 guide to water borehole installation — drilling costs, regulations, geology, contractors, and maintenance.

- Prefab & Modular Homes UK: Costs, Suppliers & 2026 GuidePrefab & modular homes in the UK: build in 3–7 months, save 10–20%, ~£1/day energy bills. Costs, 19+ suppliers, and planning for remote rural sites.